Washington Post (3/11/17), like many outlets, focused on an unrepresentative 2 percent of the American people.

The recent collapse of Republican efforts to repeal and replace the Affordable Care Act demonstrated that the GOP’s tireless obsessions—free market platitudes and tax cuts for the wealthy—contribute absolutely nothing to fixing the American healthcare system.

Unfortunately, that was the only thing made clear by media coverage of the healthcare debate.

Looking back, we are struck by the degree to which the media’s fixation on a narrative that mocks a small slice of American voters—pro-Trump voters who had new ACA coverage—deflected attention from the frustration of millions of American workers who have struggled with healthcare problems the ACA either failed to address or exacerbated.

The truth is our healthcare system is sick, and the Affordable Care Act has been little more than a bandage on a compound fracture. The ACA cut the rate of the uninsured to an all-time low, and limited the health insurance industry’s most outrageous consumer abuses, both important steps forward. At the same time, 29 million people remain uninsured, most of the non-elderly population who have employer-paid coverage are increasingly underinsured, and costs continue to soar at 200–400 percent of inflation. (See sidebar.)

Atlantic (2/23/17)

Instead of taking a serious look at the flaws in the ACA, and the deep impact they have on the lives of working-class Americans, reporters covering the healthcare repeal saga spent untold hours and column inches seeking out a tiny slice of the electorate for “reporting” that amounted to little more than mockery. Less than 2 percent of the American people both got new coverage under the ACA and voted for Donald Trump. Yet major media outlets obsessively sought out this sliver of the electorate, to ask, in the words of the Atlantic’s Olga Khazan (2/23/17),

a question that’s baffled health reporters in the months since the election: Why would people who benefit from Obamacare in general—and its Medicaid expansion specifically—vote for a man who vowed to destroy it?

Vox’s Sarah Kliff found these voters in Kentucky, more than once. Abby Goodnough and Reed Abelson did too in North Carolina for a front-page Sunday feature in the New York Times (3/7/17). Jessica Contrera found them in West Virginia for the Washington Post (3/11/17). The LA Times’ Noam Levy (2/24/17) found them in Florida. The Kaiser Family Foundation held monthly focus groups with them in Pennsylvania, Ohio and Michigan, allowing KFF president Drew Altman to opine on the Times’ op-ed page (1/5/17). Like Kliff, ABC (2/27/17) found them in Kentucky, and CNN’s Dr. Sanjay Gupta (1/6/17) went to Florida. Reporting stimulated comment from the Post’s Dana Milbank (12/20/16) to the Times’ Paul Krugman (3/14/17) to influential liberal sites like Daily Kos (1/28/17), Salon (12/15/16) and Digby’s Hullabaloo (3/13/17).

Khazan’s “baffling” question has a simple answer. Trump did not promise to “destroy” Obamacare, he promised to give people better health plans (a promise broken, obviously). Many people can’t afford ACA exchange coverage, made clear in the Kaiser focus groups:

They spoke anxiously about rising premiums, deductibles, co-pays and drug costs. They were especially upset by surprise bills for services they believed were covered. They said their coverage was hopelessly complex. Those with marketplace insurance—for which they were eligible for subsidies—saw Medicaid as a much better deal than their insurance and were resentful that people with incomes lower than theirs could get it. They expressed animosity for drug and insurance companies, and sounded as much like Bernie Sanders supporters as Trump voters.

Most people’s healthcare left out of discussion

Chart: UNITE HERE

The most damaging effect of singling out this minuscule fraction of the electorate and questioning their motives was the license it gave media to ignore the realities faced by the rest of American working families and to distort the politics of the Affordable Care Act.

Here’s who the media failed to cover: the 177 million Americans who get their insurance through job-based coverage. They are Clinton voters, Sanders voters, Johnson voters, Stein voters and, yes, Trump voters. Media generally overlook the crushing impact the ACA has had on their health insurance. To the extent people with employer-provided insurance are interviewed on healthcare, they are often wrapped in the wrong frame—that their concerns about the ACA are irrational, because the ACA didn’t impact people who were already covered.

This is just a little of what has actually happened across political, racial, economic and gender divisions to the millions of Americans with employer-sponsored health insurance since the ACA was implemented in 2010:

- The ACA imposed an excise tax on their benefits, the simple threat of which caused 73 percent of employers to cut benefits, raise out-of-pocket costs or make plans to do so.

- Their premiums went up more than 3 times faster than inflation. (See sidebar.)

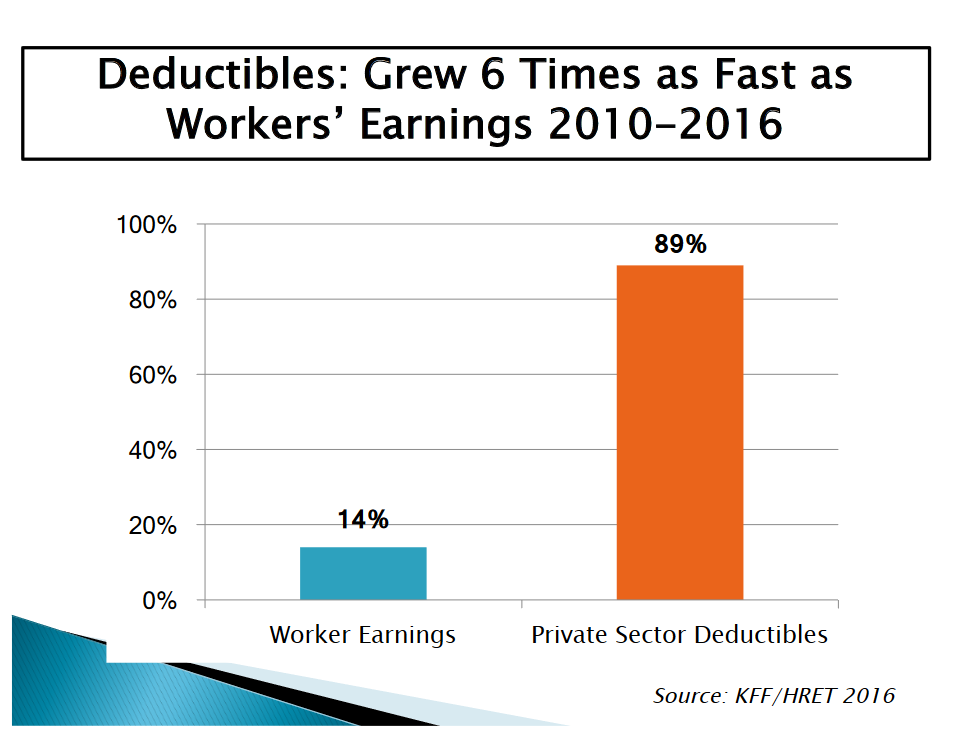

- Their deductibles increased 89 percent, while their compensation went up just 14 percent.

- When they can afford to get care, they see a stranger: 15 percent of Americans lost access to one of their doctors because their insurance network changed in just the last year.

- Even though the US has the lowest rate of un-insurance in our lifetimes, 31 percent of Americans told Gallup they either skipped or delayed necessary medical care last year because of costs, the majority for serious conditions.

- The Census Bureau reports that 11.2 million Americans live in poverty due to out-of-pocket medical expenses.

In short, the majority of Americans who get their insurance through work are facing an escalating crisis of underinsurance, brewing under the ACA and not addressed in the GOP’s proposed replacements. With more than a third of workers carrying deductibles of $1,000 or more, and 20 percent now in plans linked to Health Savings Accounts, few Americans’ benefits look much like 2010.

Shifting costs to patients

The deepest flaws in the ACA are the fruition of President Obama and congressional Democrats creating a law that counted on controlling costs by forcing employers to make American workers pay more so they would use less healthcare, instead of having millionaires pay their fair share. In particular, the misleadingly named “Cadillac Tax” is putting enormous pressure on workers’ out-of-pocket costs, based on the false notion that Americans use too much healthcare and that giving employers and workers more “skin in the game” will shrink overall costs—as if shifting costs to the least-powerful players in the system weren’t a recipe for boosting rather than curbing healthcare inflation.

In reality, we already pay more out of pocket than almost anyone else, but go to the hospital and see the doctor less often than the average for wealthy nations. American costs aren’t out of control because we use too much healthcare, they’re out of control because our healthcare system allows corporations to charge too much:

- Hospitals have been on a 20-year merger spree. Now they’re buying up doctors’ practices and charging monopoly prices for both hospital and physician care.

- Drug companies are gaming patent law and charging monopoly prices, refusing to reveal any justification for their larcenous prices.

- Insurance companies are passing provider and drug prices to their ratepayers and skimming billions of dollars off the top of an ever-growing pie.

Media focus on the actual problems with the healthcare system (e.g., Time, 3/4/13) is episodic, in contrast to the drumbeat of coverage of the political wrangling over healthcare.

These trends are covered, but only episodically compared to the avalanche of coverage of the ACA marketplaces and Medicaid expansion. The New York Times (12/15/15) and others covered a groundbreaking study of 3 billion insurance claims that showed that hospital market power and prices, not utilization, are the primary drivers of private-sector costs. Steven Brill (Time, 3/4/13) has relentlessly exposed extreme hospital prices, and pharmaceutical price-gouging is a national story (e.g., New York Times, 4/26/16). But overall, the media allows Washington politicians to frame the “reform” debate as a false choice between a status quo and Republican reaction—in other words, between a system that punishes working-class Americans and even more punitive proposals.

There are plenty of policy tools to combat healthcare corporate monopolies—from Nevada’s first-in-the-nation law curbing Big Pharma’s price-gouging on insulin, to Maryland’s successful hospital rate-setting system, to Hawaii’s employer mandate—or, of course, creating a universal Medicare-for-All (“single-payer”) system. However, all of these require politicians to put working-class Americans before Pharma, hospital and insurance industry profits. Unfortunately, few in Washington, DC, have a taste for any change that isn’t paid for by poor and middle-class families, and corporate media allow politicians to get away with it.

Republicans’ simplistic market nostrums and fixation on tax cuts for millionaires have already run smack into the brick wall of reality. The Democrats’ turn is coming. Standing back and watching GOP infighting may be satisfying, but until Democrats acknowledge the direct harm that their healthcare reforms have inflicted on American families, and the even greater harm that failing to include any restraint on the industry in the original bill has caused, Democrats will continue to suffer apparently mystifying failures at the ballot box.

The media’s myopic focus on a tiny slice of Trump voters, singled out for mockery and disdain, has enabled Democrats’ denial of the true practical and political consequences of a flawed law under whose purview the family fortunes of the majority of Americans have continued to decline.

Mike Casey is chair of the Healthcare Initiatives Task Force of UNITE HERE, a union of 270,000 North American hospitality workers. John Canham-Clyne is deputy director of research for UNITE HERE.

Sidebar:

No, Obamacare Has Not Reduced Premium Inflation

Chart: UNITE HERE

Former Obama administration officials and pundits of all ideological stripes insist that the rate at which employer-sponsored premiums have grown has slowed dramatically since passage of the ACA. It simply isn’t true.

One of the critical sources for this false fact is the Kaiser Family Foundation Health Research and Education Trust annual survey of employers. In the fall of 2015 and again in 2016, Obama White House Counsel of Economic Advisors Chair Jason Furman put out press releases linking to the survey with headlines like “New Data Show Slow Healthcare Cost Growth Is Continuing.” The White House line was picked up by pundits all over the internet.

The KFF/HRET data did show that the pace at which the nominal dollar cost of employer-sponsored premiums was growing had slowed dramatically. (For inflation, KFF/HRET uses the April not–seasonally adjusted CPI-U for all cities, available here.) But a freshman economics student knows that such information is meaningless unless adjusted for inflation.

The immediate post-ACA world includes the fallout from the economic crash, followed by the historic 2014 collapse of oil prices—eading to very low, sometimes negative inflation. A look at the actual KFF/HRET data tables reveals that from 2010 to 2016, employer-sponsored health insurance premiums grew by 326 percent of the rate of general inflation (CPI-U). For the six years prior to the ACA, premiums grew at 241 percent.

{kind=link}

—M.C. & J.C-C

Sidebar:

Factchecking the Factcheckers

The factchecking consortium’s results on ProPublica (3/22/17)

Four outlets who follow healthcare—Propublica, Vox, Stat and Kaiser Health News—teamed up to write “We Factchecked Lawmakers’ Letters to Constituents on Healthcare” (3/22/17), which stated flatly that the letters are “full of lies and misinformation.” As an example, they cited a claim to a constituent by Rep. Mike Bishop (R.-Mich.) that individual premiums are “slated to increase” under Obamacare by 73 percent, and that individual premiums for new purchasers would increase 96 percent.

The factcheckers correctly called Bishop out for citing an old 2013 study predicting that individual market premiums would be much higher upon full implementation of the ACA, and implying that it was a report on current numbers. But they went on to say:

In fact, premium increases by and large have been moderate under Obamacare. The average monthly premium for a benchmark plan, upon which federal subsidies are calculated, increased about 2 percent from 2014 to 2015; 7 percent from 2015 to 2016; and 25 percent this year, for states that take part in the federal insurance marketplace.

“Moderate”? In fact, as with employer-sponsored premiums, Obamacare premiums in the exchange marketplaces are growing at multiples of inflation:

- The 2 percent rise from 2014 to 2015 corresponded with a -0.1 percent decline in inflation.

- The ACA plans’ average 7 percent increase at the beginning of 2016 was 5 times the inflation rate (1.4 percent) for the 12 months ending January 2016.

- Leaving aside inflation, it’s unclear how a 25 percent price hike is “moderate,” but for the record, that was 10 times the 2.5 percent inflation rate for the period.

The ACA has failed to control costs and accelerated a national crisis of underinsurance. To tell readers otherwise comes across less as “factchecking” than as a partisan defense of the ACA.

—M.C. & J.C-C

This piece was reprinted by RINF Alternative News with permission from FAIR.